Futures Market: Overnight, LME copper opened at $9,396.5/mt, fluctuated rangebound initially, then dipped to $9,369.5/mt. During the session, it surged sharply and reached a high of $9,490/mt near the close, before pulling back slightly to settle at $9,469/mt, up 1.2%. Trading volume reached 17,000 lots, and open interest stood at 291,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 77,100 yuan/mt, fluctuated rangebound initially and dipped to 76,930 yuan/mt, then fluctuated upward throughout the session, reaching a high of 77,610 yuan/mt near the close and finally settling at 77,610 yuan/mt, up 1.07%. Trading volume reached 24,000 lots, and open interest stood at 181,000 lots.

【SMM Copper Morning Brief】News: (1) US January CPI inflation exceeded expectations across the board, supporting the US Fed's cautious stance on interest rate cuts. Data showed that the unadjusted YoY CPI for January was 3%, the largest increase since June 2024, while the seasonally adjusted MoM CPI was 0.5%, higher than expected.

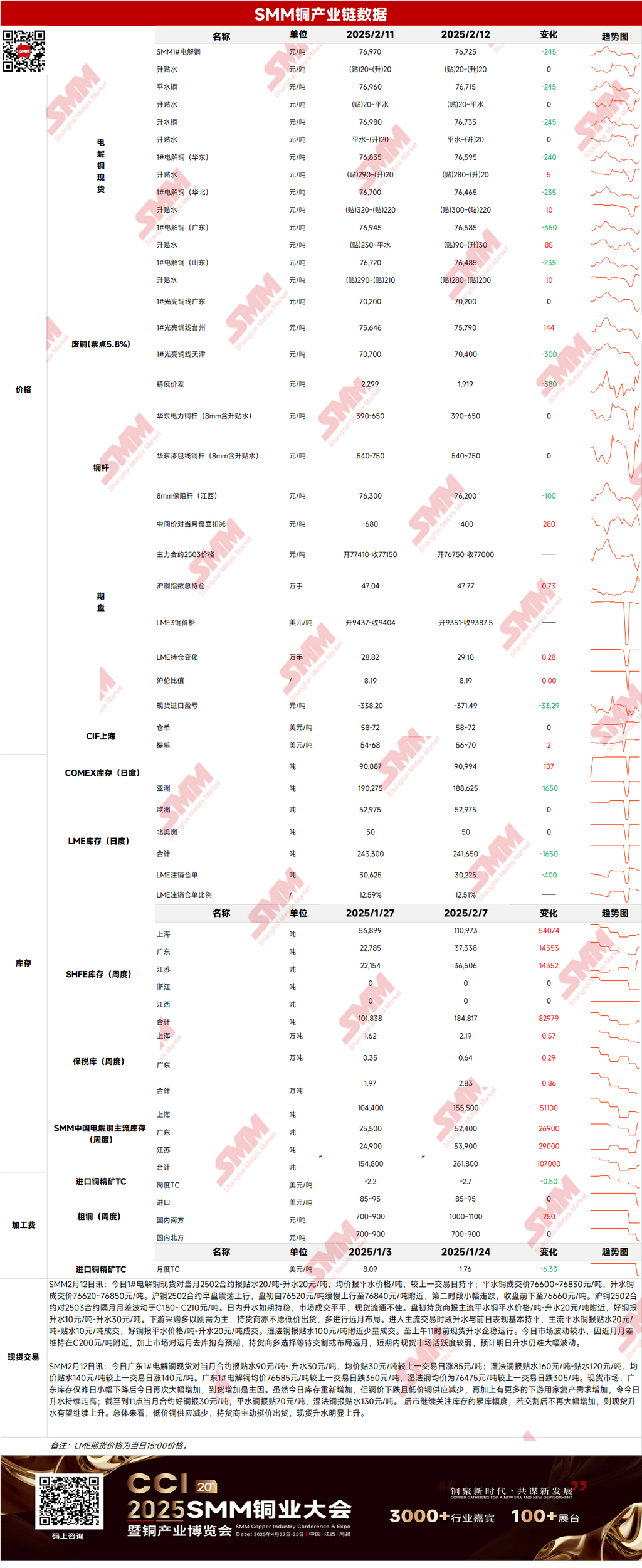

Spot Market: (1) Shanghai: On February 12, #1 copper cathode spot prices against the front-month 2502 contract were quoted at a discount of 20 yuan/mt to a premium of 20 yuan/mt, with an average price on par with parity, unchanged MoM. The market saw limited fluctuations yesterday as the price spread between near-month contracts remained around CNY 200/mt. Coupled with expectations of destocking for distant months, suppliers mostly opted to wait for delivery or position themselves for distant months, leading to weak short-term activity in the spot market. Spot premiums are expected to remain relatively stable today.

(2) Guangdong: On February 12, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 90 yuan/mt to a premium of 30 yuan/mt, with an average price at a discount of 30 yuan/mt, up 85 yuan/mt MoM. Overall, the supply of low-priced copper decreased, prompting suppliers to stand firm on quotes, leading to a significant rise in spot premiums.

(3) Imported Copper: On February 12, warehouse warrant prices ranged from $58 to $72/mt, QP February, with the average price unchanged MoM. B/L prices ranged from $56 to $70/mt, QP March, with the average price up $2/mt MoM. EQ copper (CIF B/L) prices ranged from $4/mt to $18/mt, QP March, with the average price unchanged MoM. Quotes referenced cargoes arriving in late February and early March. February mid-month cargo offers were scarce in the market yesterday, while late-month fire-refined copper B/L prices remained firm. Buyers shifted inquiries mostly to early March, with significant price differences among brands.

(4) Secondary Copper: On February 12, secondary copper raw material prices remained unchanged MoM. Guangdong bare bright copper prices were 70,100-70,300 yuan/mt, unchanged from the previous trading day. The price difference between primary metal and scrap was 1,919 yuan/mt, down 380 yuan/mt MoM. The price difference for rods was 920 yuan/mt. According to the SMM survey, the implementation of "reverse invoicing" policies still varies across regions, causing companies in provinces with stricter enforcement to face difficulties in procuring secondary copper raw materials. It will take time for adjustments before normal production can resume.

(5) Inventory: On February 12, LME copper cathode inventories decreased by 1,650 mt to 241,650 mt. SHFE warrant inventories increased by 2,696 mt to 83,999 mt.

Prices: Macro-wise, US January CPI data exceeded expectations across the board, but Powell cautioned against overreacting and maintained a cautious stance on interest rate cuts. Before Powell's remarks, Trump urged the US Fed to cut interest rates, stating that such a move would complement upcoming policies, potentially forcing the Fed to adjust rates in response to tariff policies. Additionally, two hours after the data release, Trump and Putin held a call, agreeing to negotiate an end to the Russia-Ukraine war. This news boosted the euro significantly, pressured the US dollar, and supported copper prices. On the fundamentals, the market saw limited fluctuations yesterday. The price spread between near-month contracts remained around CNY 200/mt, coupled with expectations of destocking for distant months, leading suppliers to wait for delivery or position themselves for distant months, with a low willingness to sell. On the consumption side, copper prices pulled back from highs, and downstream purchasing interest was moderate, resulting in weak short-term activity in the spot market. Price-wise, copper prices are expected to have further upside room today.

》Click to View the SMM Metal Database

【The above information is based on market data collected and comprehensively evaluated by the SMM research team. The information provided herein is for reference only and does not constitute direct investment research advice. Clients should make prudent decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】